Child custody can be a complex issue in divorce, but there’s a way to address it through tax benefits, and that’s where IRS Form 8332 becomes relevant.

Typically, the custodial parent receives tax benefits for their dependent children. However, there are situations where it makes sense for the custodial parent to allow the non-custodial parent to claim these benefits by filing Form 8332.

Form 8332 is a crucial tool for custodial parents dealing with tax matters. It allows them to transfer their right to claim a child as a dependent to the noncustodial parent. This transfer can be applied to the current tax year or future years, and it also offers the flexibility to revoke the release if needed.

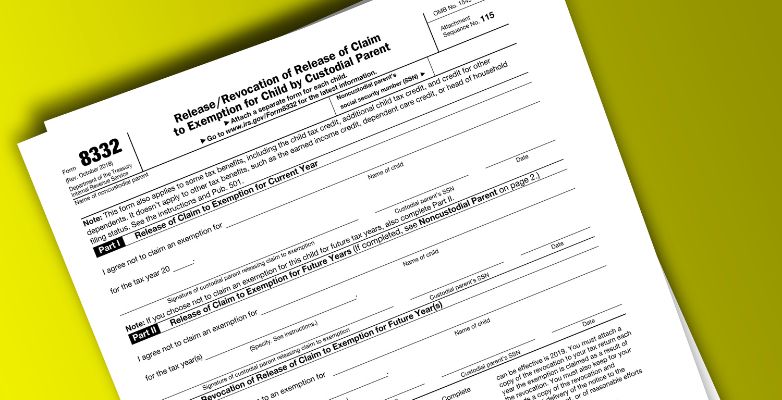

The official name of this form is the Release/Revocation of Release of Claim to Exemption for Child by Custodial Parent. While it’s true that the tax value of exemptions is currently zero until 2025 due to tax reforms, there are other significant tax benefits that a noncustodial parent can access with the help of this release from the custodial parent.

Table of Content

- 1 Form 8332 is applicable to various tax benefits, including

- 2 The Purpose of Form 8332

- 3 How to Complete IRS Form 8332

- 4 Filing Form 8332

- 5 Conclusion

- 6 Frequently Asked Questions

- 6.1 What is the purpose of IRS Form 8332?

- 6.2 Can Form 8332 be used for future tax years?

- 6.3 What tax benefits are affected by Form 8332?

- 6.4 What if I failed to file Form 8332 after claiming my child?

- 6.5 Can someone else claim my child as a dependent if I release the claim with Form 8332?

- 6.6 How can I reclaim the dependency after releasing it with Form 8332?

Form 8332 is applicable to various tax benefits, including

- Child tax credit

- Additional child tax credit

- Credit for other dependents

However, it’s important to note that this form does not apply to certain other tax benefits, such as:

- Earned income credit (EIC)

- Child and dependent care credit

- Head of household filing status

In the past, divorce decrees or separation agreements could serve as substitutes for Form 8332. However, this is no longer allowed. There is an option to create a substitute document that meets all the form’s requirements, but this can be quite cumbersome. Using the form itself is generally the easiest approach.

What if you forgot to file Form 8332 for the release of the claim? In some instances, noncustodial parents have claimed their children without receiving a signed Form 8332 or a substitute statement. This oversight could have repercussions in the event of an IRS audit, potentially leading to disallowed exemptions, child tax credits, or credits for other dependents from previous years.

Now, when someone else, like a relative (e.g., grandparent, uncle, or aunt), wants to claim your child as a qualifying child, Form 8332 is not needed for them to do so. Instead, they would need to meet specific criteria, such as the child living with them for over half of the year, among other qualifications. Additionally, the child must not provide more than half of their own support.

The Purpose of Form 8332

The purpose of Form 8332 is to allow parents to plan regarding tax exemptions for their child. Here’s what this form allows you to do if you are the custodial parent:

Release a claim to exemption for your child, permitting the noncustodial parent to claim the exemption for the child. This release also extends to the child tax credit and additional child tax credit if they apply. You can use Part I of the form to release the exemption for the current year and Part II if you want to release it for future years.

Custodial Parent and Non-Custodial Parent

- The custodial parent is typically the one with whom the child lives for most nights during the year.

- The noncustodial parent is the other parent. If both parents had the child for an equal number of nights, the custodial parent is the one with the higher adjusted gross income. There are exceptions, which you can find in Pub. 501.

Exemption for a Dependent Child

- A dependent can be either a qualifying child or a qualifying relative. You can refer to your tax return instruction booklet for detailed definitions of these terms.

- Generally, a child of divorced or separated parents is considered a qualifying child of the custodial parent. However, there’s a special rule discussed on page 2 of the form that may change this status, making the child a qualifying child or qualifying relative of the noncustodial parent for purposes of the dependency exemption, child tax credit, and additional child tax credit.

How to Complete IRS Form 8332

Form 8332 is filed separately for each child and consists of three parts. Regardless of the part(s) completed by the custodial parent, the non-custodial parent’s name and Social Security number are entered at the top.

- Part I Release Of Claim To Exemption For Current Year

- The custodial parent uses this part to release their claim to the child exemption for the current tax year, signing, dating, and attaching their SSN at the bottom. If they want to include future tax years, they must also fill out Part 2.

- Part II Release Of Claim To Exemption For Future Years

- This part is for releasing the claim to the child exemption for future tax years. The custodial parent can specify tax years or simply state “all future years” and signs, dates, and attaches their SSN at the bottom. If they wish to relinquish their exemption claim for both the current and future tax years, they complete Parts 1 and 2.

- Part III Revocation Of Release Of Claim To Exemption For Future Year(s)

- If the custodial parent decides to revoke their previous release, they complete Part 3. The revocation applies only to future years, not the current tax year.

Form 8332 is essentially a written declaration required by Section 152(e)(2) of the tax code. It allows the custodial parent to release their claim to a child-related tax exemption, provided it is:

- Signed by the custodial parent.

- Attached to the noncustodial parent’s tax return for that year.

However, Form 8332 doesn’t cover all tax benefits. Notably, it doesn’t affect the Earned Income Credit, Child and Dependent Care Credit, and Head of Household Filing Status. These have their own rules regarding eligibility.

Filing Form 8332

The parent claiming the exemption for a given tax year generally files Form 8332 with their income tax return. It’s advisable to complete this form well in advance of tax season, ensuring both parents understand the tax implications.

When Would a Custodial Parent Give Up Their Exemption?

This might be determined by court orders or support agreements. In terms of tax efficiency, the parent with the higher income usually claims the exemption to maximize tax benefits. However, income levels and phaseouts can affect this decision. A phaseout gradually reduces tax benefits as income exceeds certain thresholds, eventually eliminating them.

The child tax credit phaseout primarily impacts high-earning individuals. It applies to taxpayers with a Modified Adjusted Gross Income (MAGI) exceeding:

- $400,000 for those married and filing jointly.

- $200,000 for all other filing statuses.

For these taxpayers, the child tax credit diminishes by $50 for every $1,000 above these thresholds until it reaches zero.

Now, let’s talk about the phaseout for the Child and Dependent Care Tax Credit, outlined in IRS Publication 503, Child and Dependent Care Expenses.

Normally, this credit covers a percentage of care costs as a tax credit, with the full credit being 35% of eligible expenses, up to these maximums:

- $3,000 for one qualifying child.

- $6,000 for two or more qualifying children.

For example, if you spent $4,000 on childcare in 2022 and received the full credit, you’d get $1,400, which is 35% of your care expenses.

The phaseout for this credit starts at $15,000 (for all taxpayers except those married filing separately) and ends at $43,000. If your household has an AGI exceeding $43,000, the maximum credit becomes 20% of qualifying expenses, still within the specified dollar limits.

Special Rule for Children of Divorced or Separated Parents

In specific cases, a child is considered a qualifying child or qualifying relative of the noncustodial parent if the following conditions are met:

- The child received over half of their support for the year from one or both parents (excluding public assistance payments like TANF).

- The child spent more than half of the year in the custody of one or both parents. This can be achieved through either of the following:

- The custodial parent agrees not to claim the child’s exemption by signing Form 8332 or a similar statement. For decrees or agreements in effect after 1984 and before 2009, different rules apply (see Post-1984 and pre-2009 decree or agreement below).

- A pre-1985 decree of divorce or separate maintenance or a written separation agreement states that the noncustodial parent can claim the child as a dependent, provided the noncustodial parent contributes at least $600 toward the child’s support during the year. This rule does not apply if the decree or agreement was modified after 1984 to deny the noncustodial parent’s right to claim the child as a dependent.

For this rule to be valid, the parents must fall into one of the following categories:

- The noncustodial parent can claim the child as a dependent without any conditions.

- The other parent will not claim the child as a dependent.

- The specific years for which the claim is released.

The noncustodial parent must attach certain pages from the decree or agreement, including the cover page with the other parent’s SSN, pages containing the required information, and the signature page with the other parent’s signature and date of agreement.”

Non-Custodial Parent Must Be Eligible

For a noncustodial parent to claim a child as a dependent, they typically need to meet specific eligibility criteria. The standard rule stipulates that the parent must live with the child for more than half of the year to claim them as a dependent. However, this rule can be flexed in cases of divorce, separation, or living apart.

To qualify for this waiver, it’s crucial that more than half of the financial support for your child comes jointly from both you and the noncustodial parent. Additionally, your child should not reside with anyone other than you and the noncustodial parent for over six months in the year. So, if the noncustodial parent isn’t eligible, providing them with a completed Form 8332 won’t alter the fact that they cannot claim the child.

But handing over a completed Form 8332 entails more than just relinquishing the claim to a dependent. It also means forfeiting access to certain benefits. For instance, only the person who claims the child as a dependent can avail themselves of additional child tax credits.

Taking Your Child Dependency Claim Back

If, as the custodial parent, you decide to resume claiming your child as a dependent after releasing that claim to the noncustodial parent, you can do so by using Part Three of Form 8332. You can specify the tax years for which you’re reclaiming the dependency or simply state “all future years.” However, it’s important to note that reclaiming the dependency doesn’t take effect until the tax year following the calendar year in which you provide Form 8332 to your child’s noncustodial parent. In simpler terms, if you furnish the form in 2021, the earliest you can reclaim the dependent is on your 2022 tax return, which you’ll file in 2023.

Conclusion

In summary, IRS Form 8332 plays a pivotal role in child custody matters and tax benefits. Custodial parents can use it to release their right to claim a child as a dependent to the noncustodial parent, potentially affecting various tax credits. Conversely, it allows them to revoke this release. However, understanding its implications and complying with tax regulations can be complex. If you encounter challenges or uncertainties, don’t hesitate to seek guidance from our experts. Your child’s financial well-being is our priority.

Frequently Asked Questions

What is the purpose of IRS Form 8332?

IRS Form 8332 serves the purpose of allowing custodial parents to release their right to claim their child as a dependent to the noncustodial parent, impacting various tax benefits. It also permits the revocation of this release.

Can Form 8332 be used for future tax years?

Yes, custodial parents can use Form 8332 to release their claim for either the current tax year or future tax years. This flexibility can be valuable in co-parenting arrangements.

What tax benefits are affected by Form 8332?

Form 8332 can impact tax benefits such as the Child Tax Credit, Additional Child Tax Credit, and the Credit for Other Dependents. However, it does not affect benefits like the Earned Income Credit or Head of Household filing status.

What if I failed to file Form 8332 after claiming my child?

Failing to provide Form 8332 or an equivalent substitute statement to the noncustodial parent can have consequences during an IRS audit. It may result in disallowed exemptions and credits claimed in previous years.

Can someone else claim my child as a dependent if I release the claim with Form 8332?

While another relative may claim your child as a dependent, they would have to meet specific criteria, including the child living with them for more than half of the year. Form 8332 is not needed for this scenario.

How can I reclaim the dependency after releasing it with Form 8332?

To reclaim the dependency after releasing it, the custodial parent can complete Part Three of Form 8332, specifying the tax years they wish to reclaim or stating, “all future years.” The reclamation is effective in the tax year following the one in which the form is provided to the noncustodial parent.